If you're looking for the best business loan for your small business in the Philippines, you're in the right place. This guide breaks down your top options in 2026, from no-collateral digital loans to secured bank financing, with rates, terms, and who each loan is best for.

Many Filipino entrepreneurs still hesitate to borrow, as if taking out a loan means the business is struggling. It doesn't. The businesses you admire — the ones that scaled fast, went from sari-sari to supermarket — almost certainly used financing to get there. Debt, used strategically, is a growth tool.

Is Taking a Business Loan a Smart Move?

Taking a loan isn't a sign of failure. It's a sign that your business has reached a growth inflection point. The right loan, taken at the right time, can:

- Fund inventory before a peak season so you don't lose sales

- Hire faster so you stop being the bottleneck in your own business

- Upgrade equipment that pays for itself in productivity gains

- Open a new location while your original branch still has momentum

The key is borrowing with a clear purpose and a realistic repayment plan. If the capital you borrow generates more than it costs, it's a smart financial decision — not a risk.

What to Look for in a Business Loan

Not all loans are created equal. Before you apply, compare these five factors:

- Loan amount: Does it cover what you actually need?

- Interest rate: Monthly add-on vs. diminishing balance (diminishing is better)

- Loan term: How long do you have to repay?

- Collateral requirement: Do you need to put up an asset?

- Processing time: How fast can you access the funds?

With that framework in mind, here are your best options in 2026.

Part 1: Best Business Loans Without Collateral

No collateral loans are ideal for early-stage businesses, online sellers, and entrepreneurs who don't yet own real estate or major fixed assets. The trade-off is typically smaller loan amounts and slightly higher interest rates.

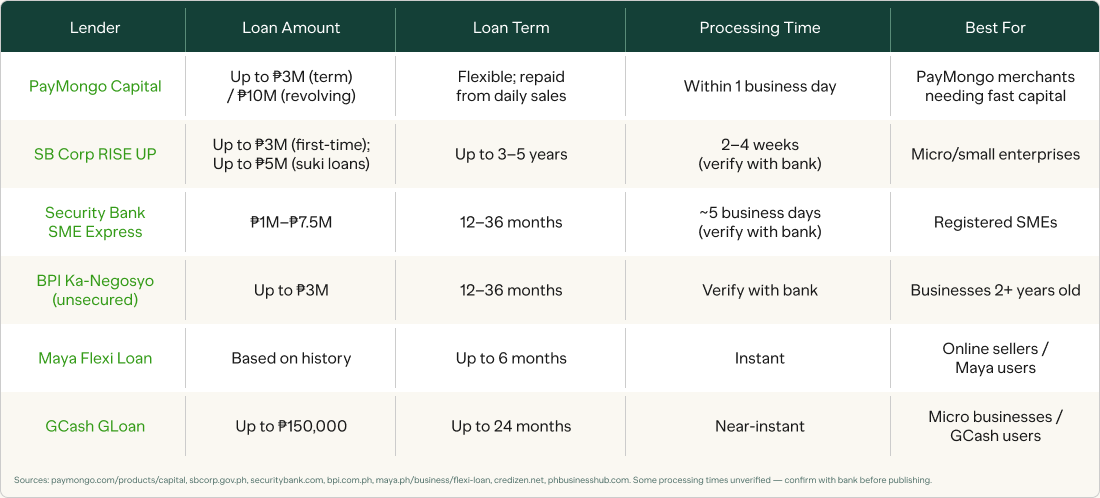

PayMongo Capital

If your business already accepts payments through PayMongo, this is the fastest and most frictionless option available. No paperwork, no collateral, no lengthy bank review.

PayMongo Capital offers funding based on your actual PayMongo sales history, so your offer is personalized to your business performance. Two products are available:

- GoTyme Term Loan: up to ₱3,000,000

- Yield Revolving Credit Line: up to ₱10,000,000

What makes it stand out:

- No collateral required. Your sales record is your application.

- Approval in as fast as 5 minutes.

- Repayment is automatically deducted from your daily eligible sales, so when sales are slow, your repayment is smaller. No fixed monthly payment that punishes you during a slow week.

- Funds in as fast as 1 business day via InstaPay/PesoNet.

SB Corp RISE UP Multi-Purpose Loan

The Small Business Corporation (SB Corp) is a government-run lender under the DTI designed specifically for MSMEs. Their RISE UP loan is one of the most accessible government programs available.

- Who it's for: Micro and small enterprises, sole proprietors, cooperatives

- No collateral for loans up to ₱3M for first-time borrowers; up to ₱5M loan amount for multi-purpose suki loans.

- Low interest rate 12% for first time borrowers, and 8-12% p.a. for multi-purpose suki loans (both based on diminishing balance exclusive of DST)

- Up to ₱5M loan amount for multi-purpose suki loans.

Security Bank SME Business Express Loan

A strong bank option for businesses that are already operating and generating revenue.

- No collateral required

- 5-7 banking days processing time

- Loan amounts from of ₱1M to ₱7.5M

- Terms from 12 to 36 months

BPI Ka-Negosyo SME Loan (Unsecured)

BPI's Ka-Negosyo loan can be availed with or without collateral, making it flexible for growing businesses.

- Available to registered businesses with at least 2 years of operations

- Minimal documentation

- Access through BPI's online banking platform

- Minimum of ₱300,000

- Loan tenor maximum of 5 years

Maya Flexi Loan (Business)

Maya's business loan product is ideal for businesses already transacting through the Maya Business ecosystem.

- Loan limits based on your transaction history

- Funds accessible instantly through your Maya Business account

- Best for online sellers and SMEs with digital payment history

GLoan

Similar to Maya, GCash offers financing tied to your GCash activity and credit profile.

- No collateral

- Can have five active loans at the same time through GLoan Negosyo

- Loan amounts up to ₱150,000.00

- Terms up to 24 months

- Interest rates 1.59-6.99%/mo (based on eligibility and chosen placement term)

- 3-5% processing fee of loan amount

No-Collateral Loans: Comparison Table

Part 2: Best Business Loans With Collateral

If you own property, equipment, or other assets, secured loans give you access to significantly larger amounts at lower interest rates. These are best for businesses in a serious scaling phase.

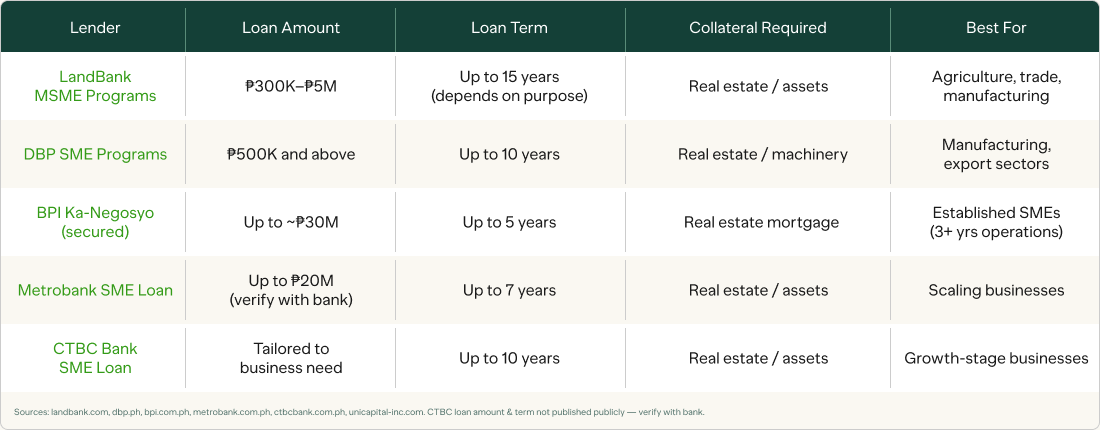

LandBank I-RESCUE / MSME Lending Programs

LandBank offers multiple MSME-focused programs with competitive government rates.

- Loan amount: ₱300,000 to ₱5M (depending on program)

- Collateral: Real estate mortgage or other acceptable assets

- Interest rates are based on current market rates.

- Terms: Up to 15 years depending on the purpose.

- Best for agriculture-adjacent, manufacturing, and trade businesses

BPI Ka-Negosyo SME Term Loan (Secured)

The secured version of BPI's Ka-Negosyo loan unlocks higher amounts.

- Loan amount: Up to about ₱30M

- Collateral: Real estate mortgage

- Terms: Up to 5 years

- At least 3 years of business operations

- Competitive bank rates with BPI's established SME support

Metrobank SME Loan

Metrobank's SME lending offers flexible structures for businesses with established financials.

- Loan amount: Up to ₱20M (verify with bank)

- Collateral: Real estate or other bank-accepted assets

- Terms: Up to 7 years, depending on loan purpose.

- Suitable for businesses with audited financial statements

CTBC Bank SME Business Loan

A strong option for businesses looking for competitive secured lending from a regional bank.

- Collateral: Real estate or other assets

- Loan amounts: Tailored to business need

- Terms: Up to 10 years, depending on loan purpose.

Secured Loans: Comparison Table

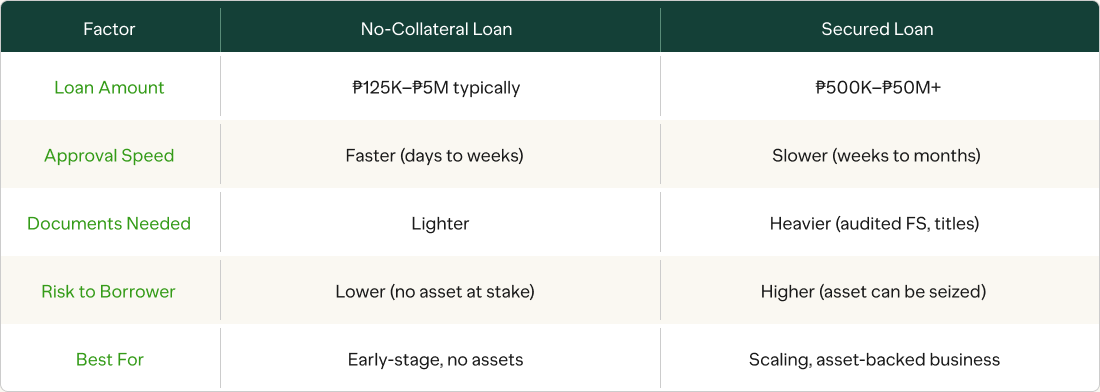

No-Collateral vs. Secured: Which Should You Choose?

Rule of thumb: If you're borrowing less than ₱3M and don't have property to pledge, go no-collateral. If you're borrowing ₱5M or more and have assets, secured loans will cost you less in interest over time.

If you're not yet a PayMongo merchant, every sale you accept through PayMongo builds your credit profile for a future PayMongo Capital loan. The more payment history you have, the larger your offer. Create a free PayMongo account and start accepting GCash, cards, and online banking — no coding required.

Frequently Asked Questions

Can I get a business loan in the Philippines without collateral?

Yes. Several lenders offer unsecured business loans, including SB Corp (up to ₱5M under RISE UP), Security Bank's SME Business Express Loan (up to ₱5M), and digital lenders like Maya and GCash. Eligibility typically depends on your business track record and creditworthiness rather than assets.

What is the easiest business loan to get approved for in the Philippines?

Digital lenders like PayMongo Capital and Maya Flexi Loan have the lightest requirements and fastest approvals – often within hours – because they assess your creditworthiness based on your transaction history.

How much can a small business borrow in the Philippines?

It depends on the lender and whether you have collateral. No-collateral loans typically range from ₱125,000 (digital lenders) to ₱5,000,000 (banks and government programs). Secured loans can go up to ₱35,000,000 or more through commercial banks and government financial institutions.

What documents do I need to apply for a business loan?

Requirements vary by lender but commonly include: DTI or SEC registration, BIR registration, business permits, bank statements (6-12 months), audited financial statements (for larger loans), and a government-issued ID. Government programs and digital lenders typically require fewer documents.

What is the interest rate for business loans in the Philippines?

Rates vary widely. Digital lenders charge roughly 1.4-2.5% per month. Banks and government lenders charge lower rates, often 7-12% per annum for secured loans, or 1% per month (based on diminishing balance) under government MSME programs like SB Corp RISE UP. Always ask for the Effective Interest Rate (EIR) so you can compare apples to apples.