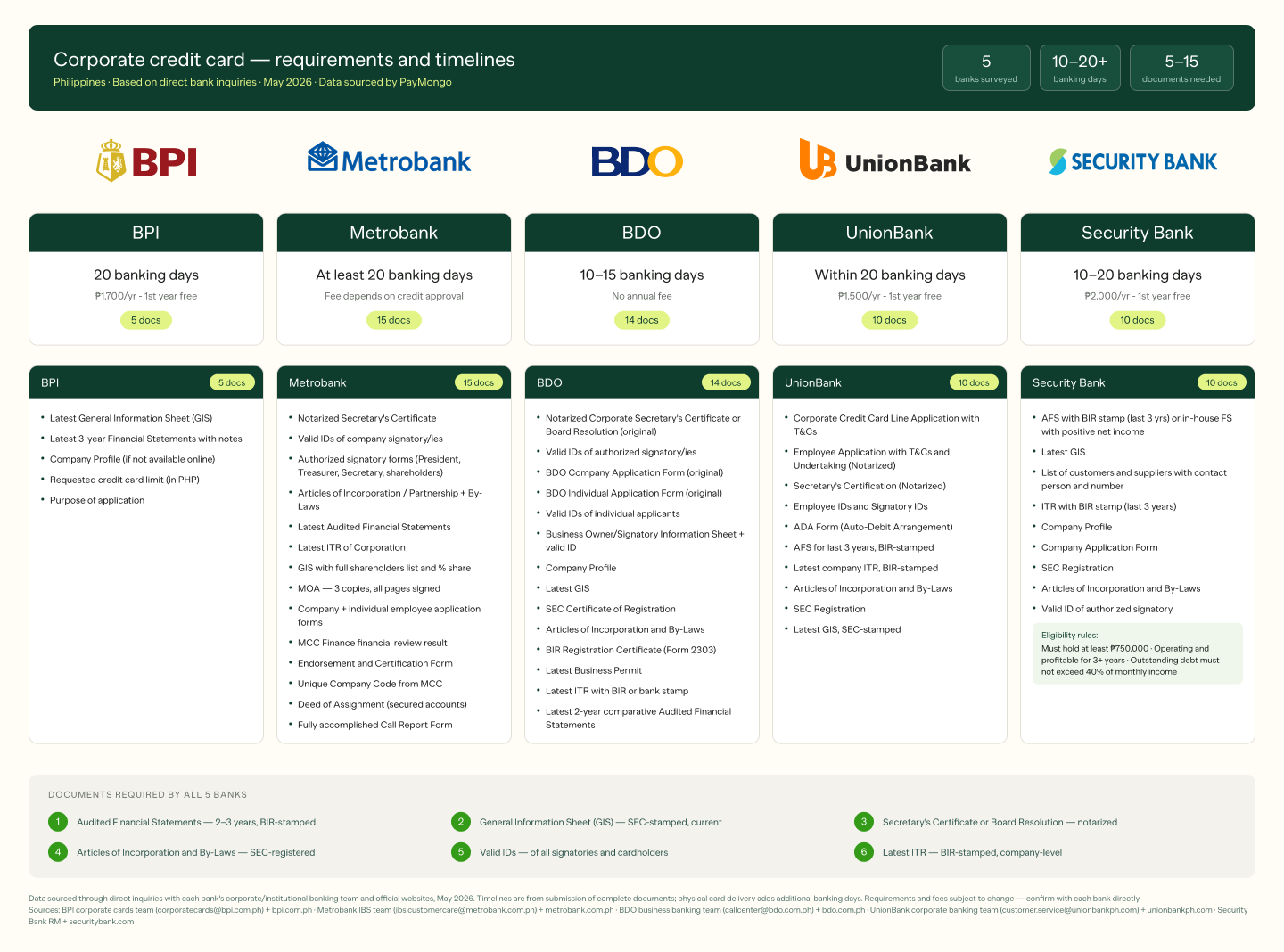

Applying for a corporate credit card in the Philippines takes longer than most business owners expect — and the requirements are more specific than a standard personal credit card. This guide covers the complete document checklist, processing timelines, and annual fees for BPI, Metrobank, BDO, UnionBank, and Security Bank based on direct bank inquiries in May 2026.

What is a corporate credit card and who can apply?

A corporate credit card is a card issued under a company's name, with a revolving credit line assessed against the business's financial standing, not any individual's personal income. It's used to separate business expenses, set employee spending limits, and consolidate billing under one company account.

In the Philippines, corporate credit cards are available to registered legal entities through bank institutional or business banking arms. They are not the same as personal business credit cards and cannot be applied for through retail branches or standard online portals.

How long does a corporate credit card application take in the Philippines?

Processing times across major Philippine banks range from 10 to 20+ banking days from the date of complete document submission. This does not include card printing and physical delivery, which typically adds another 5 to 12 banking days.

Timelines reset if documents are incomplete. The most common cause of delays is missing or unstamped Audited Financial Statements; prepare these before initiating your application.

Need team expense cards without the 20-day wait?

PayMongo Virtual Cards lets you issue cards to your team instantly, set spending limits per person, and track every transaction in real time — no AFS, no bank application, no waiting. Linked directly to your PayMongo Wallet.

Corporate credit card requirements in the Philippines (by bank)

Each bank has its own application checklist. Below are the full requirements as confirmed through direct inquiries in May 2026. Note that an existing account with the bank is needed along with the listed requirements below.

Each bank has its own document checklist. Note that an existing account with the bank is required alongside these documents.

BPI Corporate Credit Card Requirements

- Latest General Information Sheet (GIS)

- Latest 3-year Financial Statements with notes

- Company Profile (if not available online)

- Requested credit card limit (in PHP)

- Purpose of application

Metrobank Corporate Credit Card Requirements

- Notarized Secretary's Certificate

- Valid IDs of company signatory/ies (not expired, with signatures, ACR required for non-Filipinos)

- Authorized signatory forms for each of the authorized signatory/ies, the President, Corporate Treasurer, Corporate Secretary, and shareholder/s holding at least percentage share

- Articles of Incorporation/Partnership

- By Laws

- Latest Audited Financial Statements

- Latest ITR of Corporation

- General Information Sheet (including cover sheet) with complete shareholders list (with percentage share in company stocks)

- Memorandum of Agreement (3 copies, all pages signed)

- Company application form signed by authorized signatory/ies

- Individual employees application form with IDs (ACR required for non-Filipinos)

- Result of financial review done by MCC Finance

- Endorsement and Certification Form (Regional Head endorsed, if PASSED financial review; NBBS Head endorse, if FAILED financial review; NBBS Head endorsed, if requested limit is more than Php 5Mn

- Unique Company Code from MCC

- Deed of Assignment (for secured accounts)

BDO Corporate Credit Card Requirements

- Notarized Corporate Secretary’s Certificate or Board Resolution (Original Copy)

- Copy of valid ID/s of Authorized Signatory/ies bearing photo and signature

- BDO Company Application Form (Original Copy)

- BDO Individual Application Form (Original Copy)

- Copy of valid ID/s of individual applicants bearing photo and Signature

- Business Owner/Signatory Information Sheet with valid ID

- Company Profile

- Latest General Information Sheet (GIS)

- Security and Exchange Commission (SEC) Certificate of Registration

- Articles of Incorporation and By-Laws

- Bureau Of Internal Revenue (BIR) Registration Certificate (Form 2303)

- Latest Business Permit

- Latest Income Tax Return (ITR) with BIR or Bank Stamped

- Latest 2 years comparative Audited Financial Statement (AFS)

UnionBank Corporate Credit Card Requirements

- Unionbank forms: Corporate Credit Card Line Application with Terms and Conditions

- Corporate Credit Card Application –Employee with Terms and Conditions, Undertaking (Notarized)

- Secretary Certification (Notarized)

- Employee IDs and Signatory IDs

- ADA Form

- Audited Financial Statement for the last 3 years stamped by the BIR

- Latest Income Tax Return (company) stamped by the BIR

- Articles of Incorporation & By-Laws

- SEC Registration

- Latest General Information Sheet stamped by SEC

Security Bank Corporate Credit Card Requirements

- AFS with BIR Stamp for the last 3 years, or in house FS showing positive net income for the past 3 years

- Latest General Information Sheet (GIS)

- List of customers and suppliers with the contact person and contact number

- Income Tax Return (ITR) with BIR stamps for the last 3 years

- Company Profile

- Company Application Form

- SEC Registration

- Articles of Incorporation and By-Laws

- Valid ID of authorized signatory

Company requirements: Must hold amount of PHP750,000, must be operating and profitable for at least 3 years, no outstanding debt that exceeds 40% of the company’s monthly income

Documents required for a corporate credit card application in the Philippines (across all banks)

Regardless of which bank you apply to, these six documents form the core of every corporate credit card application in the Philippines.

- Audited Financial Statements (AFS):

2 to 3 years, BIR-stamped. - General Information Sheet (GIS):

Current year, listing officers, directors, and shareholders. - Secretary's Certificate or Board Resolution:

Notarized, authorizing the corporate card program and designating signatories. - Articles of Incorporation and By-Laws:

SEC-registered founding documents of your company. - Valid government-issued IDs:

Of all authorized signatories and designated cardholders. Non-Filipinos need an Alien Certificate of Registration (ACR). - Latest company Income Tax Return (ITR):

BIR-stamped, company-level.

A lot of these forms can be found in the Securities Exchange Commission's website.

Tips for a Successful Application

- Apply with your existing bank first. Banks process applications faster from existing account holders.

- Have your AFS BIR-stamped and ready before you call. This is the single most common cause of delays.

- Notarize your Board Resolution before you begin. Notarization takes time. Build it into your timeline in advance.

- Ask specifically for the corporate or institutional banking team. Retail branches and general hotlines add delays.

- Confirm the current document checklist directly with your Relationship Manager. Requirements do change. The list your RM provides in person is the most reliable.

Managing business expenses while your corporate card application is in progress

The 10 to 20+ banking day processing timeline — plus the 2–3 years of AFS most banks require — means most growing businesses go through a period where they need to manage expenses without a corporate card in place.

The businesses that come out of this period in better shape are the ones that already operate with financial discipline: clean records, separated accounts, documented transactions. These habits also happen to be exactly what banks look for when assessing your credit application.

A few things worth having in place now:

- A dedicated business wallet or account for operational transactions. Mixing personal and business spending is the most common reason SME financials look messy to a bank. The PayMongo wallet lets businesses collect, hold, and disburse funds in one place — with full transaction visibility that makes your AFS cleaner and your credit profile stronger.

- Per-person spending visibility. One of the main reasons businesses apply for corporate cards is to stop employees from pooling expenses on one card or submitting manual reimbursements. Before a corporate card is in place, setting clear per-person budgets and tracking them through a centralized tool keeps operations tight and prepares your team for the discipline a corporate card program requires.

- Documented vendor and supplier relationships. Security Bank specifically asks for a list of customers and suppliers as part of its corporate card application. Businesses that already maintain this are better positioned when the time comes to apply.

Not eligible for a corporate card yet? You can still manage business transactions through the PayMongo wallet audited financials or banking history required.

Frequently asked questions about corporate credit cards in the Philippines

How long does a corporate credit card application take in the Philippines?

Processing times range from 10 to 20+ banking days from submission of complete documents. BDO and Security Bank are the fastest at 10–20 banking days. BPI, Metrobank, and UnionBank take up to or at least 20 banking days. Physical card delivery adds 5–12 banking days.

Can a new or startup company apply for a corporate credit card in the Philippines?

Generally, no. Most banks require 2–3 years of Audited Financial Statements. Security Bank explicitly requires 3 years of profitable operations. Companies under two years old will typically not meet the financial history requirements of any major bank's corporate card program.

What is the annual fee for a corporate credit card in the Philippines?

Annual fees range from ₱1,500 to ₱2,500 per principal card. BPI charges ₱1,700 (first year free), UnionBank ₱1,500 (first year free), Security Bank ₱2,000 (first year free). Metrobank's fee depends on credit approval. BDO confirmed no annual fee.

Do I need an existing bank account to apply for a corporate credit card in the Philippines?

Most banks strongly prefer or require an existing banking relationship. Security Bank requires a minimum balance of ₱750,000. Having an existing account generally speeds up the credit assessment process.

PayMongo is regulated by the Bangko Sentral ng Pilipinas (BSP).